The LERP

A few Thoughts on the Transfer of Ownership

‘Two intelligent people cannot fall in love; true love needs one idiot’

-Fyodor Dostoevsky

I will have another note out on the Trump-Xi Summit and lack of any tangible deals, specifically, why I missed the writing on the wall so badly, the signposts to watch, and the strategic opportunity if Trump Trump’s ego can get out of Trump’s way.

Have you looked at corn futures and 10-year yields? That is NOT normal. The late week divergence should pique your interest.

Everyone was circulating this thread; the post about the forward curves, implied discounts, and capex costs are excellent food for thought. There are no direct plays in ags (to my knowledge) because they lack the depth of energy or metals, but there are certainly material impacts to margin structures as the calendar rolls forward.

We have a Rho adjustment we can put into the models, let me play with some different ideas after seeing this. High interest rates and higher corn prices will become a serious threat to ranchers if this correlation holds.

At least those Polymarket rate hike bets we put on are finally hitting.

The Fundamentals

I get the narrative - but fundamentally, if corn c/o is 1.9 z6 is 4.20. No change in my view … sure risk remains “China will buy” and “oil is high”. If one is bullish ags because of energy … you are better off buying energy. I still don’t see a grains story this year.

Days like Friday bring a lot of comments like this. If you have been bearish since $4.20 are not on board because everything will mean-revert to 20- and 30-year averages. The late week price action was great confirmation you’re correct.

The resolves won’t change until corn trades $5.50 or $6, just as nothing changed for them over the last 4 months. That’s how commodity thinking works. Agricultural markets are often the worst offenders.

StoneX printed a near 2.5-billion-bushel carry-out after the January 12 USDA report. We spent exactly one session below that price level. And remember, this was before the Iranian escalation changed the production economics for every farmer in the world.

“But bro, there’s 1.9 billion bushels on paper.”

Let’s Meet the LERP

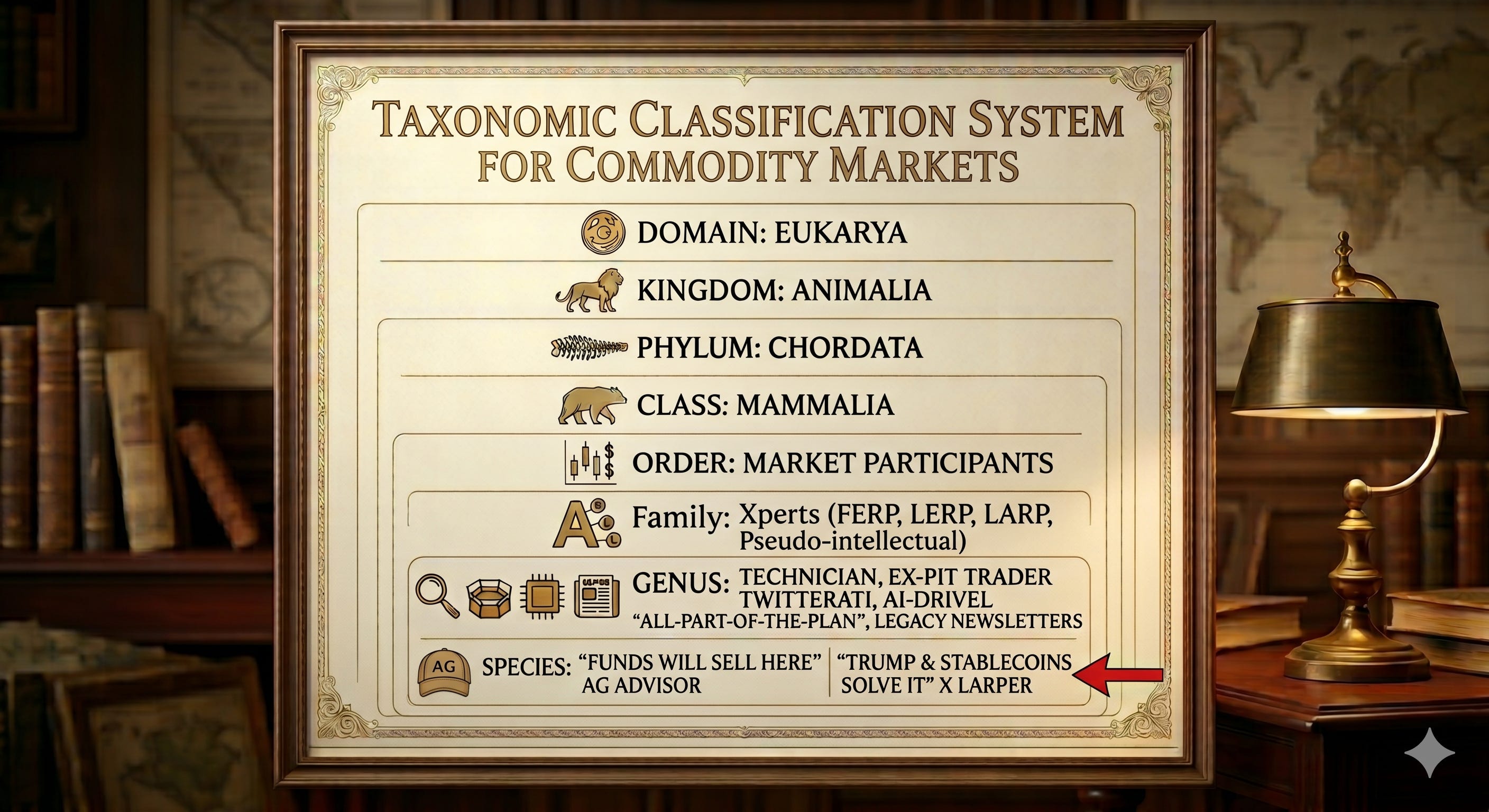

In 2026, we have identified a few of the key market participants and the purveyors of information. The LERP is the most important to understand.

Here is the broader taxonomy for this Family of intelligentsia. I like to generally refer to them as Xperts. X is a natural habitat because the algorithms (not the P&L) drive the human output; whether clicks on X or comments on LinkedIn.

“Wow, the same chart you have reposted for 23 years is very insightful. Let’s keep this back-and-forth moving in case I ever need a job. Check out my post on why my virtue signaling goes above and beyond everyone elses.”

The “pseudo-intellectualism” will, by definition, make people dumber. If your goal is to have AI generate a post to sound smart and chase millions of clicks while tracking the latest fad, it will build a reaction function that crowds in with the herd. This fuels a negative reinforcement bias to creativity and alpha.

The LERP is the Liquidity Exit Role Player.

The LERP fades the trend. The LERP is smarter than you and I. Each piece of news or brief market sell-off (or rally) is treated as the definitive beginning of the change they have called for over and over.

Naturally, any sharp break is always labeled as the beginning of the depression. We have seen this from equity bears over the last 17 years: each 3% sell-off is definitely the next 1987 or 2008 crash. Corn sells off a quarter, and it’s a new bear market. There have been four of these in 2026 alone.

The LERP is not to be confused with the FERP.

The FERP is the Farmer Expert Role Player.

The FERP uses a facade of critical insights and relationships to justify lazy work or bad processes. This is how he keeps clients while adding minimal value time and time again. The FERP is correct periodically, but what makes a FERP a FERP is a lack of self-awareness and poor processes. FERPs rarely improve.

FERP: “Corn was down because the specs were too long. I called that.”

Nicobot: “Great work bro. I hope they paid you $5 a side.”

The FERP needs clients to believe an event happened simply because he was right. This type is most commonly found in legacy newsletters and brokerage wires. Social media has bred a new genus of FERPs who are just looking for that quick dopamine kick.

This is the FERP. Yes, billion-dollar pools of capital are reorienting commodity teams and selling positions simply because an arbitrary number on a chart was breached. We can all go home now.

When I was younger, I was the largest canola/rapeseed trader in the world for a period. Softseed futures are completely dwarfed by other oilseeds futures. Every time I thought I had the market pegged, something would shift in the world soybean S&D. I was of course “right” as my P&L got wrecked. We are never right when the P&L goes down.

It’s no different when the largest soybean oil producers go from driving prices to getting steamrolled by palm or heating oil shocks.

Anyone who has traded seriously knows that nothing we say or do actually impacts these markets.

LERPs and FERPs love strong statements:

“The funds can’t buy anymore.” “Managed money is caught and will have to sell.”

A common trait of the LERP is the facade of an alpha trader coupled with strong directional statements. He is consistently wrong, only to celebrate each time the price corrects. Whether he actually entered a real trade is, much like the FERP, anyone’s guess.

But the critical difference is that the LERP is a material market participant. We all risk becoming LERPs—exit liquidity for others—when we fight trends and markets.

Specific to a niche like ags, the LERP pretends to swing a big directional stick while usually carrying small positions or proxies. What I mean is that they are “short the spreads” or holding puts in an ETF.

The LERP goes from months, years, and in special cases (like equity bears and gold bugs) even decades of being wrong, to obnoxiously celebrating each minor victory as if it were all part of the plan. Do you see the online overlap of the LERP and the LARP? Hence members of the same Family.

A recent example is the Nico-LERP when I shorted bean oil earlier this year. Bean oil has rallied 50%, but there was a week in there when prices sold off hard. I doubled down on the belief that this EPA would not create an impossible demand mandate that would drive prices higher across the board. Boy, was I wrong.

The LERPs footprint in the market happens in two steps:

They become exit liquidity to the guy taking profits.

Then becomes the next leg of the trend higher (lower) when they stop out.

This is exactly why we need the LERP.

Negative Alpha is a Multiplier

What makes LERPs enigmatic is that, in some cases, they are highly intelligent and eventually right.

Peter Schiff, Ray Dalio, and Michael Burry are fabulously successful. Together, they have called 3,427 of the last 2 recessions. If you listened to them over the last two decades, you underperformed crypto bros, Treasuries, and Cathie Wood. Brutal list.

I was a LERP when I started financing a losing position because I knew better. Because we do our own work, I’m always at risk of smoking my own stuff and becoming a LERP the day the P&L stops dictating “right from wrong.”

Here’s an easy test: when you make a statement, put on a paper trade (assuming you didn’t make the actual trade). If you ignore the P&L just to make noise, you are a LERP. If you never intended to make the trade, you were already a FERP.

The Intersection is a Signal

It is when we see these two intersect that you should always consider adding to a profitable position. The FERP does not have a position. The LERP is the fuel for the next leg higher (or lower).

The more obnoxious the victory laps, the better.

We shared this note on April 23, 2026, when the FERPs and LERPs all got aligned because of positioning from the Commitment of Traders (COT) Report—the laziest of lazy analysis. Corn longs jumped to their highest level since early 2025. I made the video below about why this is nonsense, and we added to corn length.

Friday’s close was still 1.5 cents higher.

This week in corn was an example of what happens when the exit liquidity is gone. We need the LERPs; without the LERPs, it’s time to reduce positions or even consider stepping aside.

Since I only speculate, I am the most vulnerable long. I need the LERPs to rollover, or the speculators to develop their own reasons to buy. The other commodity buyers and sellers have serious staying power (bank products, ETFs, hedgers, producers, end-users, etc.).

We can still laugh about the facade of it all. It is when the LERP joins the trend that we need to become more vigilant.

Across ags, the LERPs jumped in following the USDA report’s 180-degree pivot and the same hope I had for a broader China deal. Here is the caveat, it was not the LERPs I expected.

Transfer of Ownership

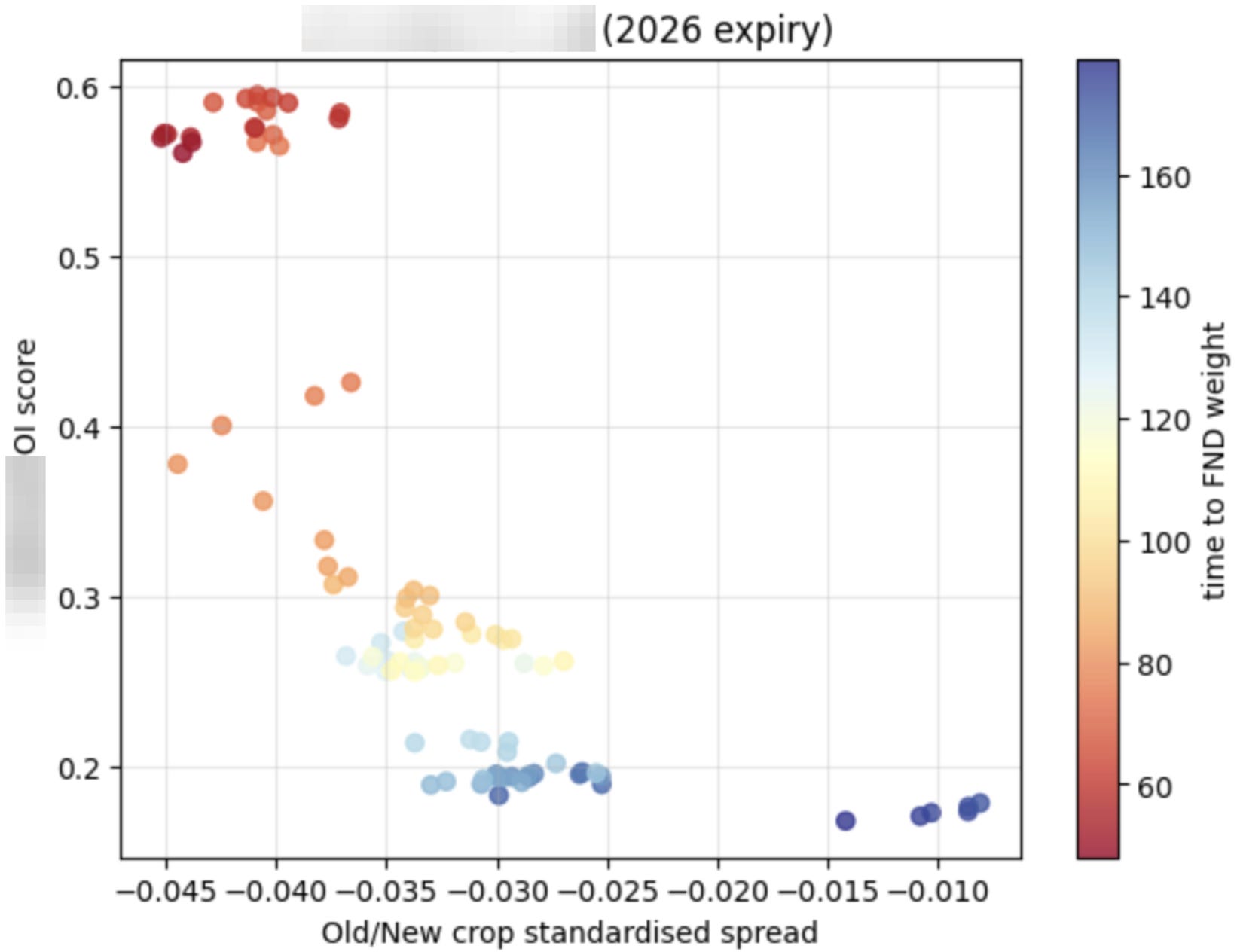

This week saw a massive transfer of ownership across the corn, wheat, and oilseed product markets. The wheat figures especially intrigue me.

The path of the corn market confirms a massive amount of complacency and some heavy positioning. Moves higher will feel like slogs, unlike cotton and wheat. We will dig into this below.