Peckish

Survey Conerns Front and Center

"The world is split between those who do not sleep because they are hungry and those who do not sleep because they are afraid of those who are hungry."

—Paulo Freire

"Peckish" means feeling slightly or mildly hungry, often indicating a need for a small snack rather than a full meal.

I wake up at 4 AM, and this is what the screen looks like. I’m feeling peckish. This is the proverbial snack: picking away at positions, adding to others, and taking profits where the market gives them to you. Bullish or bearish, there’s a trade for everyone with this type of volatility (uncertainty). We will increase our total length while remaining respectful of the weather forecasts, which improved Monday to Wednesday as the GFS shifted toward the ECMWF—meaning wetter in central and southern Brazil.

590P OZWK9 at 32% Impvol is still juicy

CTZ6 >200 pts off the Z highs.

ZCZ6 is still hanging out below $5

KEK6 setting back /w $6.40 in its sights

ZL prices 125 pt daily moves vs ZS at 10

ZSK6 ATM impvol <15%

One reason to remain “peckish” and spread across commodities is that we don’t have the slightest clue how this situation will evolve. I like this chart from Jim, but it serves as a reminder: if you want to trade macro thematics as a basis for agriculture, you will be data-light. It’s the “Da-Ta Wasteland” after all.

Surveys Shouldn’t Break Our 💔s

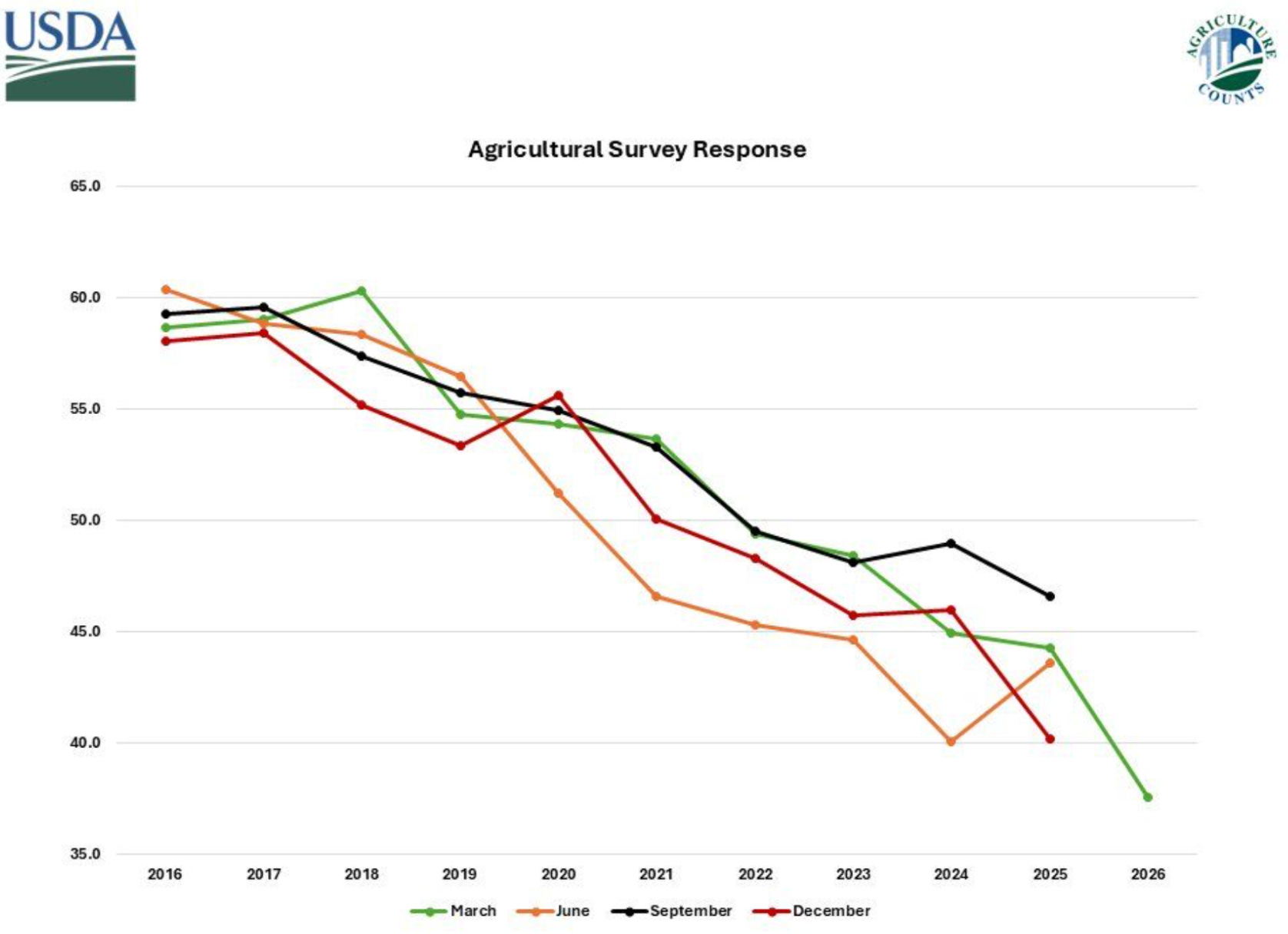

This is from a note last July. We pointed out why private companies mimicking unreliable surveys at a fraction of the size were not useful. It isn’t only these surveys; we are increasingly in the habit of discarding the USDA conclusions because of everything highlighted below and more.

Trust in this process belongs in 2005. Many companies effectively create a mishmash of methodologies and forecasts that offer no way to isolate or improve existing biases and errors.

We ignore most of these private surveys because we were aware of these issues years ago. It’s well documented across all USDA industries: livestock, cotton, dairy, and others. Even at the most basic methodology level, the best companies will have the same embedded biases, only much more concentrated.

When we forecast USDA reports, we focus on three criteria:

What we think the USDA will say & how the market will interpret it.

The real economics —> shows where the miss is most likely to come from.

Does it change how we will trade?

The Two Ways to Approach Summer 2026

The first approach: Traditional Ag Traders - King Corn

Think of these as traditional newsletters and the crowd that “blames the algos.” Mostly operate under existing assumptions. Keep digging for anecdotes that suggest “King Corn” is more confirmation of what we already knew. The U.S. farmer has favored soybeans over corn exactly once in history.

Market your crops and stay short. Hold the line.

“King Corn” has nothing to do with trading this market. It will serve as confirmation bias for whatever gets printed—nothing more, nothing less.

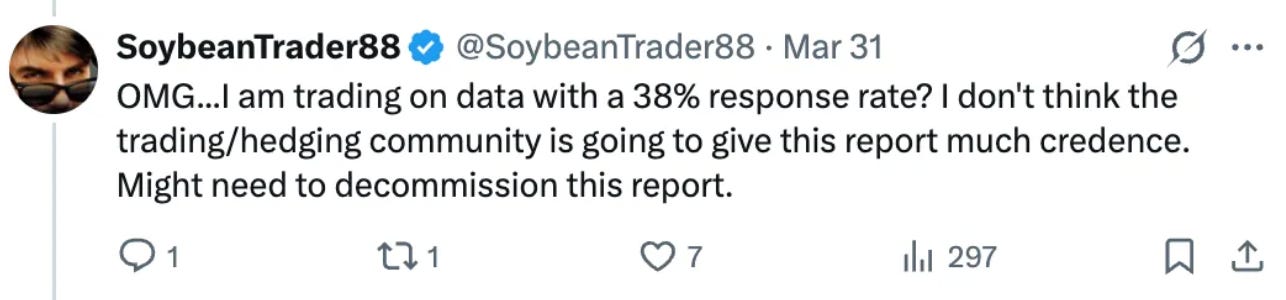

Recognize that the data is susceptible to greater error due to the low response rate. SoybeanTrader’s faux-realization is valid, but TINA (there is no alternative).

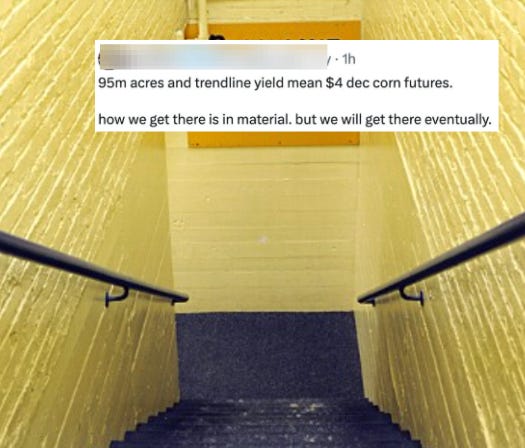

Traders will spin it or ignore the evidence anyway. Let’s take a look at this gem.

“How we get there is in material” is my new favorite phrase. It shall be enshrined in trader lore—possibly the silliest trading comment uttered on social media.

The entire point of this profession is to identify the path price takes to affect the underlying supply and demand before arriving at its final definition. People in the first camp are forced to utter cliches that raise deeper philosophical questions: What are we even trying to accomplish here? lol

The Second Approach: Price Action Doesn’t Match the USDA

Recognize that price action and world events do not suggest this is a typical contango or mean-reverting market that demands minimal risk premia.

Most people can at least agree that this is not a reliable report after the UDSA put the response rate front and center. My first question is “why now?” Why did the USDA choose this report to make clear that the response rate was so poor? We’ve known this after all.

Embedded Biases

I will lead off with the big one because this is what people will find most controversial: there are non-economic drivers, making this specific report difficult to analyze—more so than the typical weather and policy “known unknowns.”

For every “back to the Stone Age” dumb tweet, there are insightful posts. Here’s one. It was a simple way to say the point I intended to make, “ummmm I think people made a decision because of how they ‘felt’ and that’s hard to prove. Let’s try to isolate some data that makes this more than a finger-in-the-air guess.”

I also suspect Lance & Co did us a favor when they put the industry on notice: