No Heatwave, No Catalyst: Ag Prices Slide on Trade Uncertainty

AiQ July Summary

“Simple can be harder than complex: You have to work hard to get your thinking clean to make it simple.”

— Steve Jobs

July in Review: Data & Context Makes Wx Simpler

AiQ Pegs Corn Yield at 184.7 — A Record Crop, But What’s the Delta?

The 800-lb Gorilla: Nighttime Temps and Corn Sweat

See Something, Say Something: Bad Weather Takes

Biggest Weather Risk? The Black Sea. And We Will Watch China Closer

Argentina Makes History. First Permanent Tax Cuts in Decades

Trade Deals Galore: Does it Matter for Ag?

AiQ Planted the Flag July 19, 2025: Dating—not Marrying—our Trades

Q3/4 Thematic: Inputs Are Not Coming Down, Costs Will Rise

A Trainwreck in Progress: AI Is a Double-Edged Sword

I recently learned what TLDR stands for. Lightbulb—I am always TLDR for some. Let’s be proactive. It’s a monthly summary. Break it into pieces. This one is free. Please provide feedback. Thanks for reading.

Lazy Work & What Funds Actually Do

The yield controversy on social media was—once again—predictably absurd. In classic ag fashion, rather than engaging with the quality or accuracy of the work, defenses were based on passions, and hopeful no one actually knows what more sophisticated players do. Spoiler: “hedge funds” don’t do lazy work.

FYI, the three largest Hedge Fund platforms—with multi-strat characteristics—now account for over 30% of volume in certain markets. Their growth isn’t accidental. If you’re running a $10B+ equity book and consistently pulling double-digit returns, why wouldn’t you extend the edge from those strategies into commodities?

Their alpha is built on applied math, real-time data, and massive computing power. Forget weekly USDA updates and condition ratings—they're scraping everything from railcar loadings to credit card transactions as they happen.

This is the modern playbook. Public data is the backfill—no longer an edge.

Success is a double-edged sword. There is the cyclical challenge of needing to reinvest more following each year of profitability. Hence, the cascade of money into commodities and alternative investments.

Hedge funds struggle to maintain performance as assets grow and strategies get more crowded. The recent rise of “congestion” strategies speaks for itself. The latest equity rally has been fueled by the retail crowd since Liberation Day… The bull market was getting long in the tooth.

One of the most crowded trades has become short-term volatility selling—arising from retail interest in owning 0DTE options. Today, these account for 60% of options traded on the S&P. The unsurprising outcome is compression of volatility spilling into commodity markets.

This is not unique to agricultural markets, commodities, or equities. As the President calls for 200 and 300-point cuts and experts warn the long end will break, bond market volatility grinds to the lowest levels since early 2022. Volatility compression is happening across most markets.

This is why it’s important to understand what hedge funds actually do. They have the latest technology and need to deploy capital in alternative assets to limit the crowding-out effect. Commodities are forced to absorb an increasingly larger share.

AiQ’s Yield & Corn Sweat Update

AiQ pegs the national corn yield at 184.7 — A record crop, but what’s the delta? Together, the precipitation and temperatures imply yields on the top end of the range, 186.6. More nuanced data indicate a higher risk this summer, attributed to the magnitude of the overnight temperature rise. I was not very familiar with this phenomenon until a few weeks ago. Let’s explore the data in specific states facing the strongest anomalies.

Below are AiQ’s state-by-state yields. You can get the full report at the link here.

A month ago, we highlighted what was needed for a July weather story. We got zero out of three.

The 800-lb Gorilla: Nighttime Temps and Corn Sweat

A reader highlighted the post below from a few weeks prior. He is correct, my attitude toward the noise was laissez-faire. I wasn’t aware that nighttime temperatures, corn sweat, evapotranspiration, etc., were essentially the same thing. Then, in mid-July, areas of the country ratcheted up.

Once I went through the data, two items caught my attention.

A few states appeared to be underperforming, considering the strong topline temps and precip.

When I dug into the data, 2025 was more of an outlier than I thought. In some cases, locally, and in other cases, statewide.

The models appear to underperform at a national level, but there is inconsistency state-to-state. Pennsylvania is experiencing its most extreme year in decades. Yet, our models suggest it can still set a new record. Is the answer, it should have been even bigger? Either way, ZP871 is correct; our concern level has changed—And this is why we stay humble and react to the data accordingly.

Keep in mind, we are still predicting a record crop by a considerable margin, and there is no corn story.

“See Something, Say Something”

The problem with meteorologists is that they have to talk about the weather. See something, say something—but instead of calling out true anomalies, they treat 7 to 10 ordinary things as if each were extraordinary.

We’ll cover this more fully in a dedicated note.

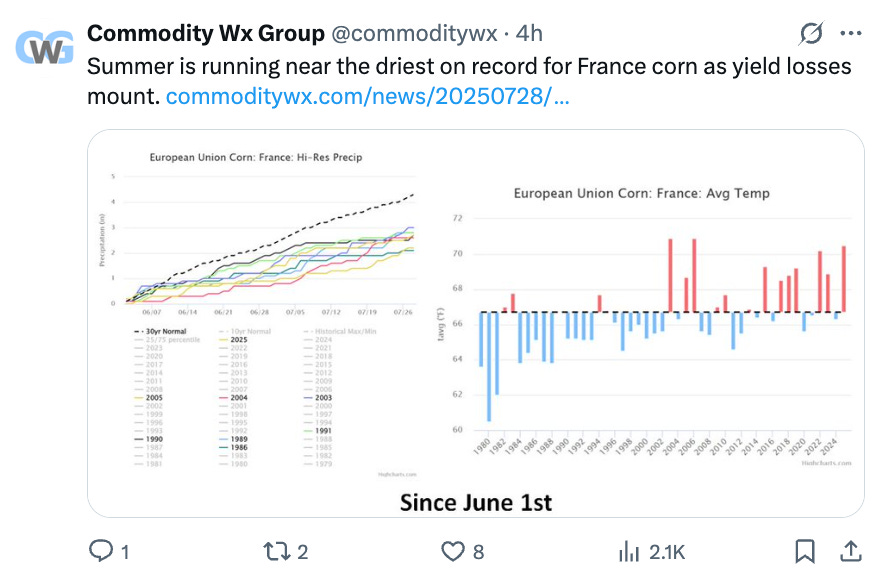

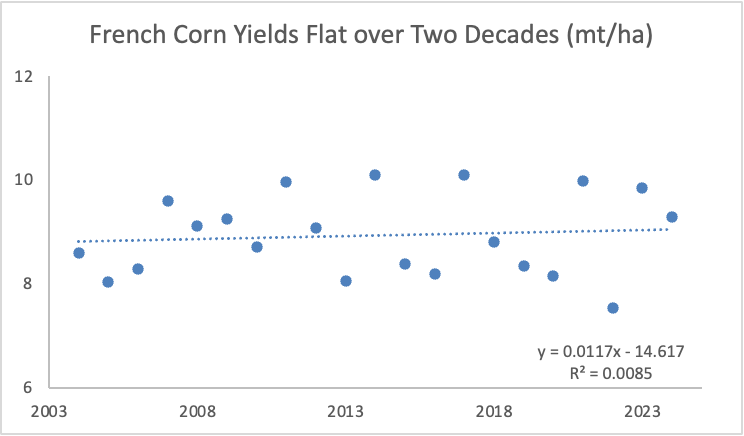

This post caught my attention. I saw something and had to say something—because I have to ask: Why are they signaling as if the situation in France is a catastrophe?

Markets are prescient; they usually sniff out these stories. Does Matif wheat look like it’s concerned?

Nouvelle-Aquitaine, France’s largest growing region, has been extremely dry—31% below normal since June. Yet long-term precipitation remains slightly above average, which may or may not matter. Certainly helps. Daily highs are running 6.4% above normal, just under 2 standard deviations—roughly 1-in-15 to 1-in-18-year events. In short: very hot, very dry.

Pays de la Loire, in the northwest, saw the second-hottest summer on record (+7% daily highs), with precipitation at 88% of normal—a hot summer following decent spring rains, but the hardest-hit region overall.

Moving east, Grand Est had 93% of normal precip and above-average temps, placing it in the bottom quintile of the past 40 years. Auvergne–Rhône-Alpes fared better, hitting 100% of normal precip and posting its second-best long-term moisture profile. Still, temps were 4–5% above normal.

History points to yield losses in the 4–7% range. But even satellite signals conflict:

NDVI implies one of the worst seasons ever

VHI shows a crop closer to average

If you were penciling in 9.2 mt/ha (trend 9.1), is it now 8.8? 8.7? That’s roughly 4% below trend. The states I ran through cover roughly 2/3 of France’s corn production.

If you prefer the excitement of meteorology hyperbole, then by all means.

FRANCE COULD BE THE WORST EVER. THANK YOU FOR YOUR ATTENTION TO THIS MATTER 😂😂😂

Biggest Weather Risk? The Black Sea. And We Are Watching China Closer

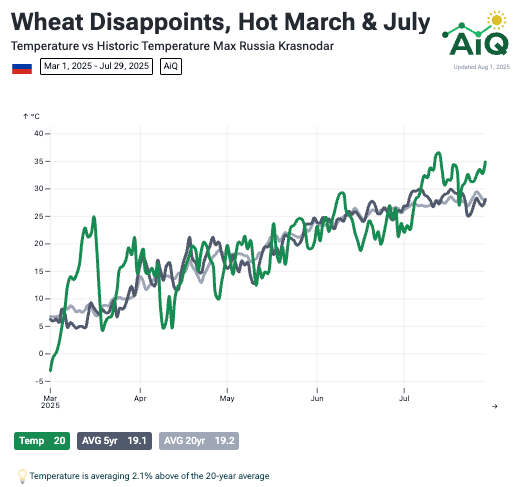

Harvests in Ukraine, Romania, and Russia are all trending disappointing. Bulgaria got torched. Regional balance sheets—tightened further by low Turkish stocks—will head into 2026 under pressure. Near-term market impact is limited, but harvest pace should accelerate.

In Russia, reports from Krasnodar and Rostov show ~30% YoY yield declines, offsetting improvements in Volga and Tambov. AiQ pegs the Russian crop at 82 MMT, a 1.5 MMT cut from last month.

Other red flags: Russian and Ukrainian sunflower crops. Ukrainian data looks better than anecdotal reports suggest, despite late winter freezes, drought, locusts, and conflict. AiQ holds wheat at 22 MMT, with 1 MMT downside risk.

Corn remains the wildcard—some analysts (not deeply embedded) are slashing to 25–26 MMT, but we see 27–29 MMT as more realistic. Total grain output likely lands 1–2 MMT below 2024.

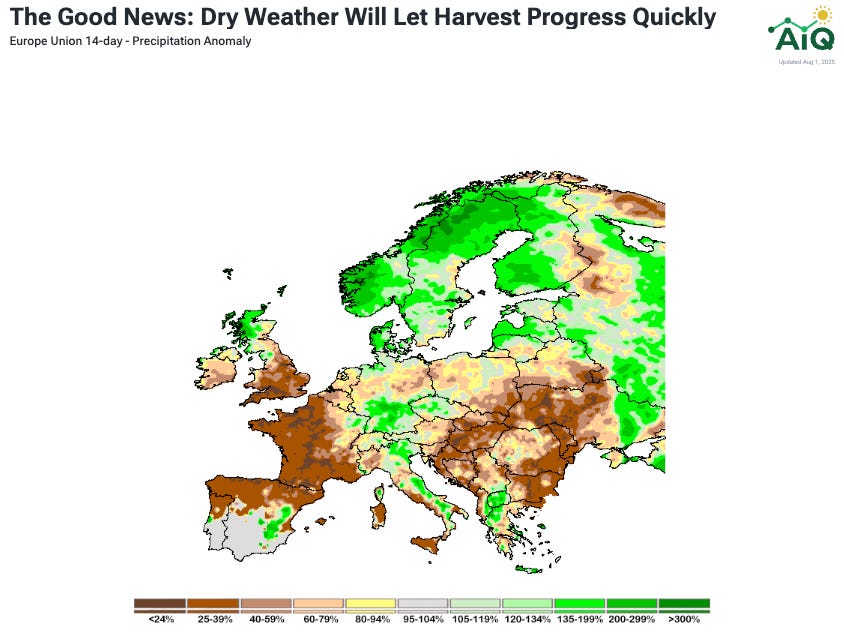

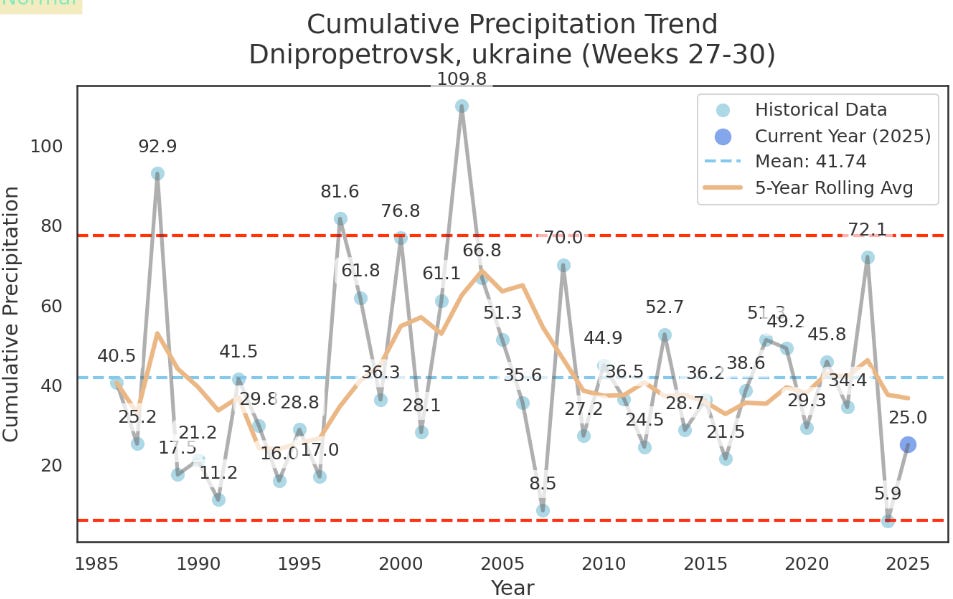

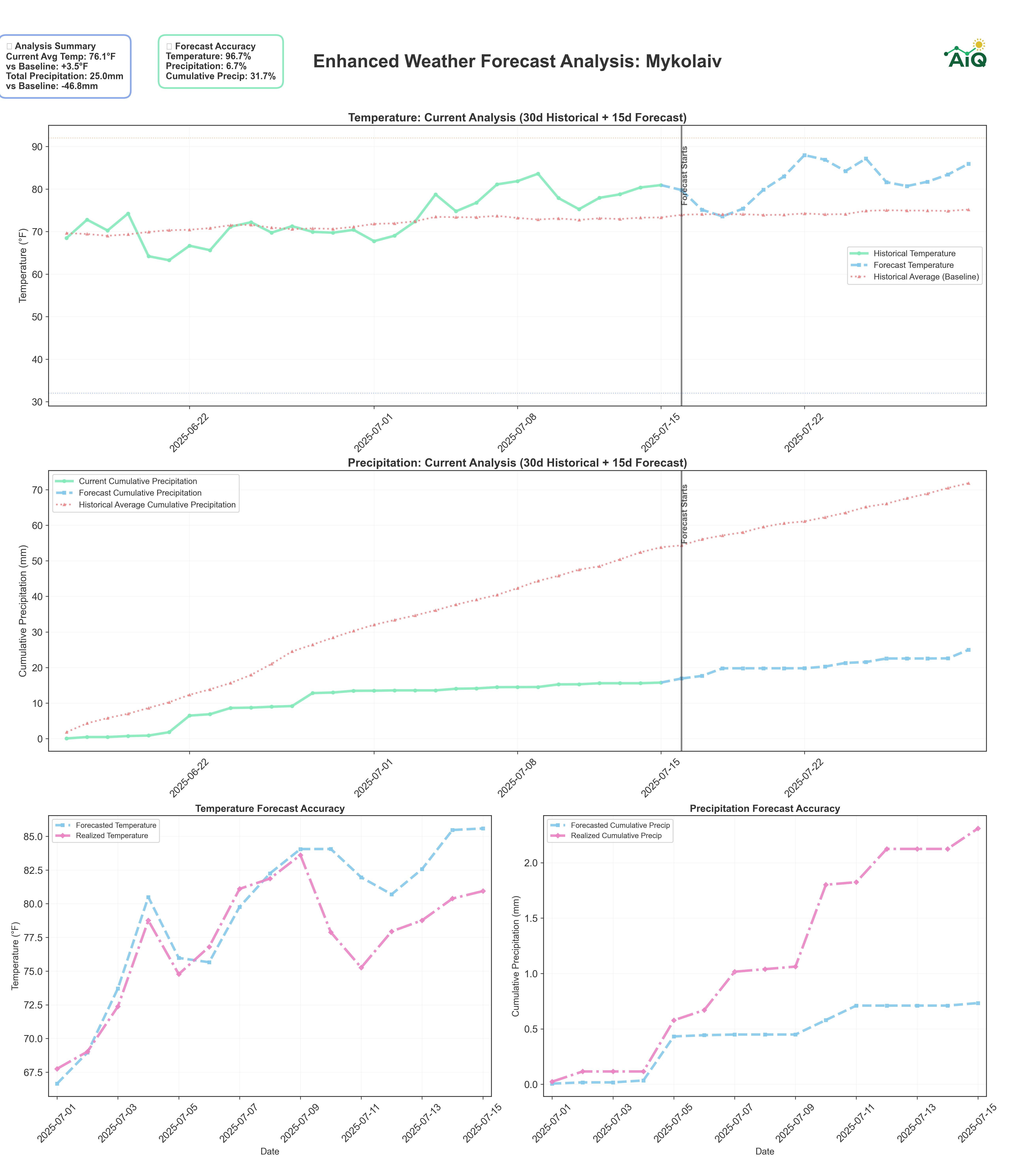

Photos of Ukraine Showing Devastation are Likely from Mykolaiv

Below is one of many posts getting shared across social media. Mykolaiv is a large agricultural state, and it has been most affected by the drought this year. See AiQ’s 30-day realized and 15-day forecast image below.

Shifting to the East—China

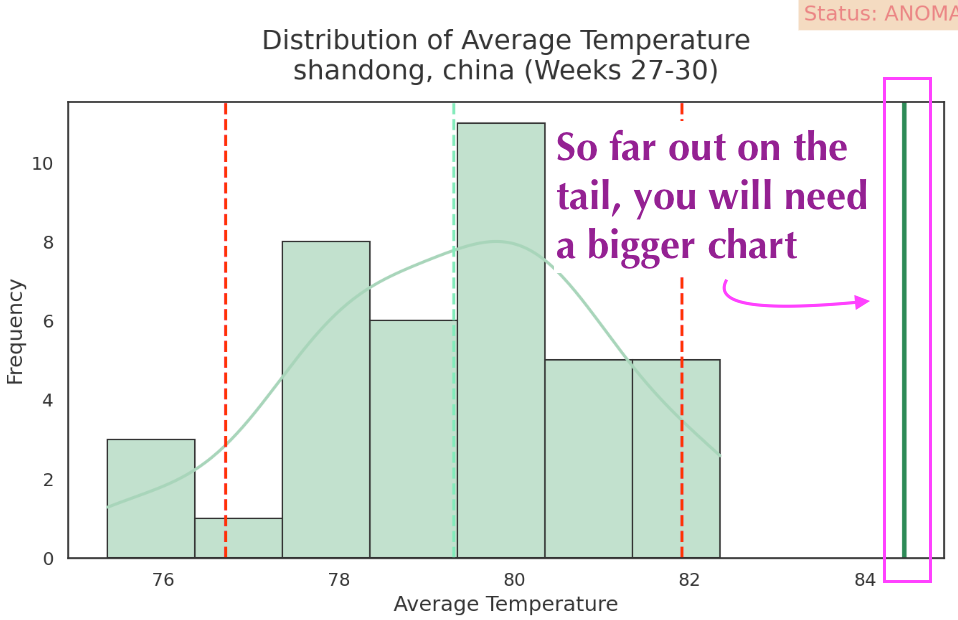

AiQ has lowered its Chinese corn production estimate by 5 MMT (295), aiming to align it with last year's production. Persistent heat and recent feedback drove the revision. Of course, official numbers remain inflated, and models are only as good as the data, so interpret cautiously. Local feedback is not optimistic on better yields in the Northeast, offsetting challenges elsewhere.

The takeaway: After last year’s record crop, China may no longer be building stocks—a notable shift, even if not yet actionable. This area of eastern China accounts for 30% or 80 million tonnes of corn production.

Argentina Makes History. First Permanent Tax Cuts in Decades

Here were the tax reductions and key points from the announcement. The BCR expects a $28 billion increase in farm income over the next decade as a result. This was a better outcome than we expected (pre-announcement note here).

Poultry and beef will be reduced from 6.75% to 5%, corn from 12% to 9.5%, sorghum from 12% to 9.5%, sunflower from 7.5% to 5.5%, soybeans from 33% to 26%, and soybean by-products from 31% to 24.5%.

"From the avalanche of problems, only the heaviest anvil remains: the tax cuts. That's why I want to make an important announcement about this great scourge that should never have existed.”

“We seek to boost the agricultural sector, which has been severely punished by these taxes over the last 20 years. I repeat, these reductions are permanent and cannot be reversed while I am in office. Eliminating withholding taxes is an obsession for our administration, and we have made significant progress in that direction,”

“It is important to keep in mind that this is solely thanks to the fiscal surplus we have achieved, which we guard like water in the desert against the systematic attacks of the political class.”

-J Milei July 26, 2025

Excellent visual from Javier on how much more farmers will get paid for soybeans today—26% more per tonne than the end of June. I have two questions.

Did the government make a mistake cutting soybean taxes to 26%, while products stay elevated at 31%? Will soybean exports continue as China buys non-US origin beans? Traders seem to have missed the BCR already cut crush from 43 to 41.5 million tonnes. Paraguayan beans are being shipped to Brazil, rather than their usual route to Rosario.

Farmers sold enough in late June to meet cash needs and hold the over. Now, with the government signaling further tax cuts, there’s even less incentive to sell.

Yes, existing tax burdens and expensive domestic credit still matter. But with the board trading below $10, and no immediate pressure, selling likely stays muted in the near term.

Analysts in Rosario now expect next year’s planted area to jump 8%, up sharply from flat projections before the policy announcement.

Outside of CBOT pricing, July was the best month in years to be a farmer in Argentina—and they haven’t felt that way in a long time.

Trade Deals Galore: Does it Matter for Ag

Short answer: No. As long as the US pushes the world toward higher trade barriers and uncertainty, agricultural prices will find it difficult to rally.

As we outlined in our mid-July trade notes (here and here), U.S. agriculture continues to be sidelined in global trade talks—for a simple reason: agriculture matters more to our trading partners than it does to us.

Take the recent South Korea deal. Announced 24 hours before the deadline, it touted a $350B headline figure—mostly driven by shipbuilding contracts. But these ships will be built in South Korean yards, not American ones. The rest of the “investment” is mostly repackaged earlier commitments from the Biden administration.

And on agriculture? Nothing. No movement on rice or beef—the two sectors U.S. farmers care most about. Why? Because South Korean farmers were prepared to protest, and Seoul wasn’t willing to pay the political cost. Washington wanted a win. Agriculture was an afterthought.

In our mid-July notes, we explained exactly why this outcome was predictable—and why similar dynamics will keep playing out.

Now look at Brazil. Ahead of new U.S. tariffs, Brazilian farmers were clearly nervous (see FT article excerpt). Yet when the tariffs came, key ag exports—like orange juice and wood pulp—were exempt, while others like coffee and sugar were not.

There was no logic or consistency behind the choices.

White House advocates argue that this erratic approach is strategic. We disagree. What we see is that agriculture repeatedly gets left behind, because it's more vital to the other side and less valued in U.S. trade priorities, even amid broader policy unpredictability.

India’s Trade Policy is the Definition of Circular Contradiction

India runs a $100 billion trade deficit—unlike China, it is a net importer. One of the core issues U.S. trade policy should target is China’s excess manufacturing capacity, which continues to crowd out global competitors. This is where U.S.–EU-Japan-India-Canada-Mexico alignment should be strongest.

India, meanwhile, is one of the few countries with the potential to serve as a regional counterweight to China—and a long-term growth hub for U.S. companies seeking alternative supply chains and demand expansion.

Yes, India has significant trade barriers, but context matters:

Over 100 million farmers, with another 150 million indirectly dependent on ag

Per capita GDP: $2,700 vs. China at $13,500 and the U.S. at $89,000

Instead of building alignment, U.S. policy mixes geopolitical, military, and trade goals—and risks failing at all three. Trump wants to penalize India for buying Russian arms, yet offers only more expensive U.S. alternatives with strings attached. He targets trade barriers while publicly attacking U.S. companies investing in India.

This approach risks driving India back toward China—a country it isn't naturally aligned with—because Trump offers no viable alternative. And crucially, India isn’t dependent on the U.S. consumer the way China is.

AiQ Planted the Flag July 19, 2025: Dating—not Marrying—our Trades

Back on July 19, we flagged it’s time to start looking at ag commodities from the long side. Our bellwether? Cotton—not because of strong fundamentals, but because price action was firm and the chart appeared to be carving out a multi-year bottom. A classic contrarian setup off an early-season low.

We’re not advisors—we build tools to help navigate timing, because in the real world, timing beats good ideas. In a downtrending, policy-driven market, the worst mistake is getting married to a position. This is when you date the trade, not commit.

That said, we like the long-term bull case for cotton.

U.S. ending stocks may be overstated by ~1 million bales

Planted acres could be revised as soon as next week with the FSA update

Producers don’t have an incentive to plant at lower prices

The $45 crude target from May seems a distant memory

The downside looks limited, but as always, markets have a foul sense of humor—so tread lightly.

We also highlighted soybeans, noting long-term support in the $9.80–$10.20 range, where traders could take shots with 300–400 bps of risk. The seasonality was running 4-6 weeks ahead all spring.

The past two weeks delivered a fairly bearish set of events:

Improved July/August weather. Record US crops are the modal scenario.

Trade war volatility as tariff rates reach their highest in nearly a century.

Minimal cutouts or support for US agriculture, the DXY needs to help.

A more optimistic South American production outlook after currency devaluation and tax cuts.

Here is what to watch:

US cattle are in the process of a long-term top.

Sugar should be on your radar below $16.

Cocoa areas of Africa are raining, the chart will test support after it established a clear trendline lower.

Has palm oil has found support in the 4,200-4,300 ringgit area?

Here is what you need to be watching in early August

Wheat, corn, soybean meal, and other ags are cheap—and they should be. Back-to-back record crops, with buyers in no rush to step in, create ideal conditions for rolling short vol and spread trades. A catalyst is needed.

We don’t sell crops below the cost of production, so there’s not much to do down here. Traders don’t need my help capturing a carry.

The real risk? Geopolitical escalation.

The Russia–China trade timelines hit in just over a week.

How hard does Trump press Putin?

Will the U.S. push the Middle East to pump more oil and undercut Kremlin revenues?

Does Trump risk his current detente with Beijing to eliminate Putin’s support?

Meanwhile, Washington and Beijing are at a standstill. Does it hold—or does the President turn up the heat to isolate China from Russia?

Today’s risk-off tone might be less about the payrolls print—and more of a warning shot for what’s coming next.

Q3/4 Thematic: Inputs Are Not Coming Down

The theme commanding our attention is cost of production. U.S. and Brazilian costs aren’t falling. In fact, Argentina may be the only place globally where producers could be materially better off six months from now than they were six months ago.

Cost sets the floor. Prices can dip below it—but not for long. And now, we’re finally approaching that floor.

A Trainwreck in Progress: AI Is a Double-Edged Sword

We are big fans of AI. We use it each day. We demonstrate how data and AI improve profitability for businesses and decision-making for humans across our space.

Stuck in the Past: Why Ag Must Accelerate Its AI Adoption (June 17, 2025)

Having said this, “AI investments” are crowding out the real economy, while people race headfirst into the trap of mindless consumption. The AI race—getting all products to market first and endless resource consumption—is a societal liability, too.

“Why cut interest rates?” I expect there are two distinct goals:

Reduce interest expense for the federal government.

Goose the wealth effect (my explanation here).

You can talk about mortgages and small businesses, the drivers of the REAL economy, but those are not why POTUS is fixated on Powell. Meanwhile, Meta and Microsoft adding hundreds of billions in market cap in a day, or Nvidia minting new billionaires, does nothing for Main Street.

So the question is: Why do it? What’s the upside for all Americans?

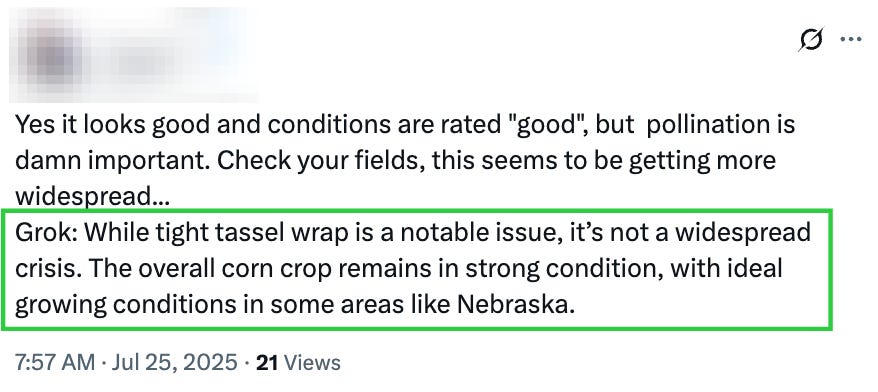

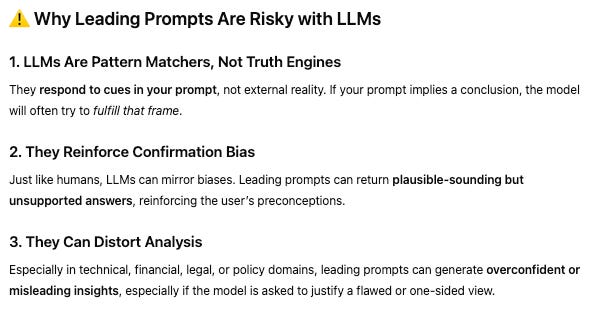

It should be obvious that AI can make us think less—but it’s worth calling out just how flawed it is to ask a model like “Grok” about rare or unprecedented ag risks.

We're talking about problems that can't be modeled: a seed variety that fails in humidity, for example. These aren’t in any database. Yet people ask LLMs trained mostly on social media, which is full of clickbait, hyperbole, and half-truths.

You could hardly do worse.

How could anyone on X differentiate when something becomes a “notable issue,” is it actually hurting yields—or just going viral? Hint. Hint. It’s the latter.

Either way, anything more than a social media post requires research and data to support the claim.

This is how a tool becomes a crutch. Don’t outsource your thinking with a leading prompt to a bot that wasn’t developed to provide a reliable answer.

August is upon us. Stay disciplined.

Thank you for reading. Please reach out to Nico@archaiq.ai with any suggestions on how to improve our products or if you're interested in exploring new opportunities with ArchaiQ. Sign up for our free weekly newsletter at www.archaiq.ai. Each morning, we will add some daily notes to our Substack chat (link here).

This is not trading or investment advice. Trading Futures is a high-risk activity; please consult with a professional.